Every real estate agent has encountered their share of challenging Clients, each presenting unique hurdles to overcome.

Take a look at this story shared by a real estate agent in the USA.

Phone Rings.

I answer.

A guy is calling from a listing sign, and he doesn’t know where he is.

He can’t read the agency name — he blames the sign — and he can’t describe the property for crap. He starts getting really impatient with me, but I finally get enough information to McGyver his location by intuition and the hard science of assuming he’s looking at one of our cheapest listings because of his demeanor. I am right, and after I answer his basic questions about the home’s layout, this conversation ensues.

Caller: “How much is the rent? I’m interested in making it my home.”

Me: “Sir, the house is not for rent. You can only buy it.”

Caller: “Well, that’s dumb. Why did you put the sign here, then?”

Me: “I’m not the agent listing the house. [Agent] is out of the office, but the sign clearly says, ‘For sale,’ with the number to get assistance right away.”

Caller: “That’s why I called. I want the house, and I’ll pay rent on time.”

This goes around and around, with me using analogies comparing buying versus leasing in other situations like cars and equipment. Trying to make him understand makes it worse.

Me: “If you really like it, I will have an agent get in touch with you to show you the inside and explain the buying process. Remember, though, it can’t be rented. The owner only wants to sell it.”

Caller: “Look, idiot, I know this may be hard for you to understand, but I just want to rent it. I think I can come up with the $130,000, but I need to know what the rent will be after that. It shouldn’t be hard for an educated person to figure out.”

I once again try to explain loans, mortgages, and buying a home.

Caller: “So, what happens after I come up with the money? I won’t get a loan like you tried to sell me on; that sounds like a scam, and I don’t want to pay rent to a bank. What will I be paying per month, and who do I pay it to?”

Me: “So, you’re wanting to buy the house for cash? And now you want an estimate of the monthly costs? Is that right?”

I start pulling up Excel to estimate closing costs and taxes.

Caller: “Yes, finally, you understand. I need to know what the rent will be.”

Me: “That is not called rent. Those are monthly expenses, not rent. If you pay cash to buy the house, you won’t have a rent payment; you’ll be the home’s owner. You’ll only pay the taxes and utilities if you occupy it, and you’ll have to pay closing costs and title insurance.”

Caller: “So, you mean if I pay cash, I won’t pay rent? Just that other stuff? What about cable?”

Me: “That’s up to you. Nobody is forcing cable on you.”

Caller: “This sounds great. Tell me more. This will be cheaper than I thought.”

Me: “Is this a joke? This is [My Boss], right? You’re hazing me or something?”

Caller: “I have no idea what you’re talking about. Back to cable…”

Me: “You can hire a company to mow your lawn, get a satellite dish, or anything you want as long as it’s not illegal or against neighborhood rules. It’s your house to decide what services you want.”

Caller: “Those are great ideas. And I’m going to rent this house. You are smarter than I thought. God bless you, son. Jesus loves you. Praise the Lord, I can retire!” *Hangs up*

In this story lies a reflection of the challenges and triumphs that define the daily lives of real estate professionals and it serves as a reminder of the importance of patience, communication skills, and adaptability required to guide clients through the intricacies of property transactions.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been published from Not Always Right on July 2023.

For informative news and views on the world of real estate, proptech and AI, follow overwrite on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog

overwrite | real estate content creation, reimagined

From Bloggers to Vloggers to Tik-Tokers, the real estate industry has ridden every social media wave. But this week, we’re diving into the world of Podcasts. While it’s not the freshest face in the crowd, savvy agents are turning to this medium in growing numbers and unlocking the secrets of success in the ever-evolving real estate world.

Dubai Property Podcast provides you valuable information about the real estate market in Dubai. Including property investment, property management, market trends, legal requirements, and comprehensive information if you are looking to buy or sell property in Dubai, as well as for real estate agents and investors.

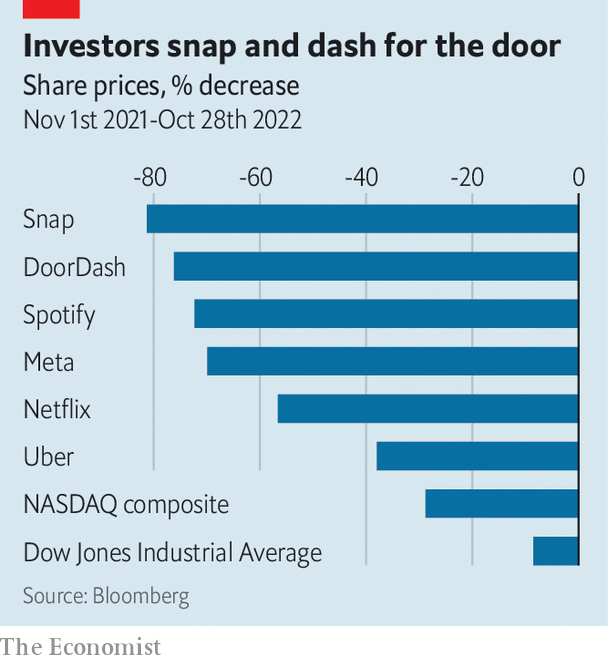

Despite superficial differences, digital darlings’ business models rest on the same shaky pillars.

When evan spiegel, boss of Snap, wrote in a leaked memo that the social-media company had been “punched in the face hard by 2022’s new economic reality”, he might as well have been describing America’s digital darlings as a whole.

After a multi-year bull run, the sector is suffering a sharp correction.

The nasdaq index, home to many consumer-internet firms, has fallen by nearly 30% in the past 12 months; the Dow Jones Industrial Average, made up of less techie firms, is down by less than 10%. Crunchbase, a data provider, estimates that American tech firms have already shed more than 45,000 jobs this year.

Macroeconomics is partly to blame. Soaring inflation and rising mortgage repayments are leading consumers to cut back on discretionary spending—and most digital offerings are discretionary.

Even the industry’s trillion-dollar giants have not been spared, despite continuing to rake in handsome profits. Alphabet, Amazon, Apple and Microsoft have collectively lost $2trn in market value over the past 12 months.

The movers, the streamers and the creepers

If you think big tech has it bad, spare a thought for the not-so-big tech. In particular, three business models embraced by firms born after the dotcom crash of 2001—and subsequently by investors—are losing steam: the movers (which shuttle people or things around cities), the streamers (which offer music and tv online) and the creepers (which make money by watching their users and selling eerily well-targeted ads). Over the past year, the firms that epitomise these business models—Uber and DoorDash; Netflix and Spotify; and Snap and Meta (which has tumbled spectacularly out of the trillion-dollar club)—have shed two-thirds of their market capitalisation on average.

And things could get worse. Despite being the global leader in ride-hailing, Uber on November 1st reported yet another quarterly loss. In its 13-year life it has torched a cumulative $25bn of cash, equivalent to roughly half its current market value. DoorDash, the leader in food delivery, also remains lossmaking. So do Spotify (despite decent revenue growth) and Snap (in addition to sharply slowing sales).

Netflix—a child of the 1990s but a streamer only since 2007—turns a profit but its revenue growth was down to 6% year on year in the third quarter, compared with a historical average of more than 20%. Meta’s revenues have now shrunk for two consecutive quarters.

On the surface, the movers, streamers and creepers—and thus their problems—look distinct. On closer inspection, though, their businesses all turn out to face the same main pitfalls: a misplaced faith in network effects, low barriers to entry and a dependence on someone else’s platform.

The network effects

Start with network effects, or “flywheels” in Silicon Valley speak—the idea that a product’s value to a user rises with the number of users. Once the user base passes a certain threshold, the argument goes, the flywheel powers a self-perpetuating cycle of growth. It also explains why so many startups seek growth at all cost, spending millions acquiring ever more customers to get the flywheel spinning.

Network effects are real. But they also have their limits. Uber believed that its headstart in ride-hailing gave it a ticket to riches, as more riders and drivers would mean less idle time for both, drawing ever more users into an unstoppable vortex. Instead, it encountered diminishing returns to scale: reducing average wait times from two minutes to one would require twice as many drivers, even though most riders would barely notice the difference. DoorDash’s hungry consumers likewise only require so many alternative Indian restaurants to choose from. And what network effects the movers enjoy are local; a user in New York cares little about the popularity of the app in Los Angeles.

The Netflix Movie scored a rare 0% audience rating on Rotten Tomatoes

Spotify and Netflix also tried to capitalise on network effects, as oodles of data on the listening and viewing habits of similar users promised to deliver an unbeatable product. Belief that Netflix’s trove of user information would give it a winning edge in creating content has been shattered by flops like “True Memoirs of an International Assassin”, which scored a rare 0% audience rating on Rotten Tomatoes, a review website. For the creepers—whose social networks are a network-effects business par excellence—the worry is what happens if the flywheels start spinning in reverse. Meta had a scare in the fourth quarter of 2021, when it lost 1m users. That loss did not turn into a stampede; the company has added users since. Next time it may not be so lucky.

From Boon to Bane

The second problem—low barriers to entry—also looks like a supposed boon that turned into a bane. Advances in technology, from smartphones to cloud computing, allowed all manner of startups, including the movers, streamers and creepers, to build consumer software cheaply and quickly. But that also meant that copycats soon emerged, and easy money allowed them to offer generous discounts to quickly build the minimum necessary scale.

Fending off the rivals

Although Uber faces only one real ride-hailing rival, Lyft, in its home market, its global expansion almost immediately ran up against local rivals such as Didi in China or Grab and Gojek in South-East Asia.

The combination of relatively simple products and free-of-charge user experience means a new twist on social media can be enough for a new challenger to gain momentum: just try to pry a teenager from TikTok.

The barriers to entry for the streamers are higher—Netflix and Spotify spend a lot of money making or licensing content. But they are not insurmountable, especially for deep-pocketed rivals. To fend off the challenge from Disney, which is spending a total of $30bn a year on content, Netflix has to keep splurging, too, to the tune of around $17bn a year. Like customer-acquisition costs for the movers, content costs eat into streamers’ profits. Disney’s streaming services lost $1.1bn in the second quarter of this year and the company has said that its Disney+ platform expects to lose money until 2024. Heavy investment explains why Netflix’s free cashflow (the money companies generate after subtracting capital investments) is equal to only 6% of revenue.

Is the clock ticking for TikTok?

The third flaw common to the three wobbly business models is their reliance on distribution platforms that are not their own. Uber and DoorDash pay a handsome fee to advertise on the iPhone and Alphabet’s Android app stores. Spotify forks over a 15% commission on subscriptions purchased on iPhones—a tax so annoying that it has filed a complaint against Apple over it. Netflix avoids the commission by forcing users to subscribe through their web browser, shifting the irritation to the customer—and quite possibly missing out on subscriptions.

Worst affected by the lack of their own rails are the creepers. Their dependence on the iPhone-Android duopoly is an existential threat. Apple’s newish requirement that users give iPhone apps permission to track their activity across other apps and websites, a move since replicated by Alphabet, may this year cost Meta an estimated $10bn in forgone revenue. Parler, a creeper favoured by the far right for its liberal attitude to speech norms, was temporarily suspended by both Apple and Android. If American national-security hawks worried about TikTok’s Chinese ownership get their way and force Apple and Alphabet to expel it from their app stores, the rising star of social media could find itself similarly thwacked.

The different business models do not face an equal balance of challenges. The movers would be in better nick if the industry had meaningful barriers to entry. The streamers may have been able to bat away new entrants if network effects had been stronger. And the creepers were in reasonable shape until Apple and Alphabet spoiled their party. One shaky pillar is problematic enough. Three of them is a disaster waiting to happen.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been repurposed from an article published online in The Economist on 31st October 2022, without modifications to the text.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our NewsBites blog, updated weekly.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

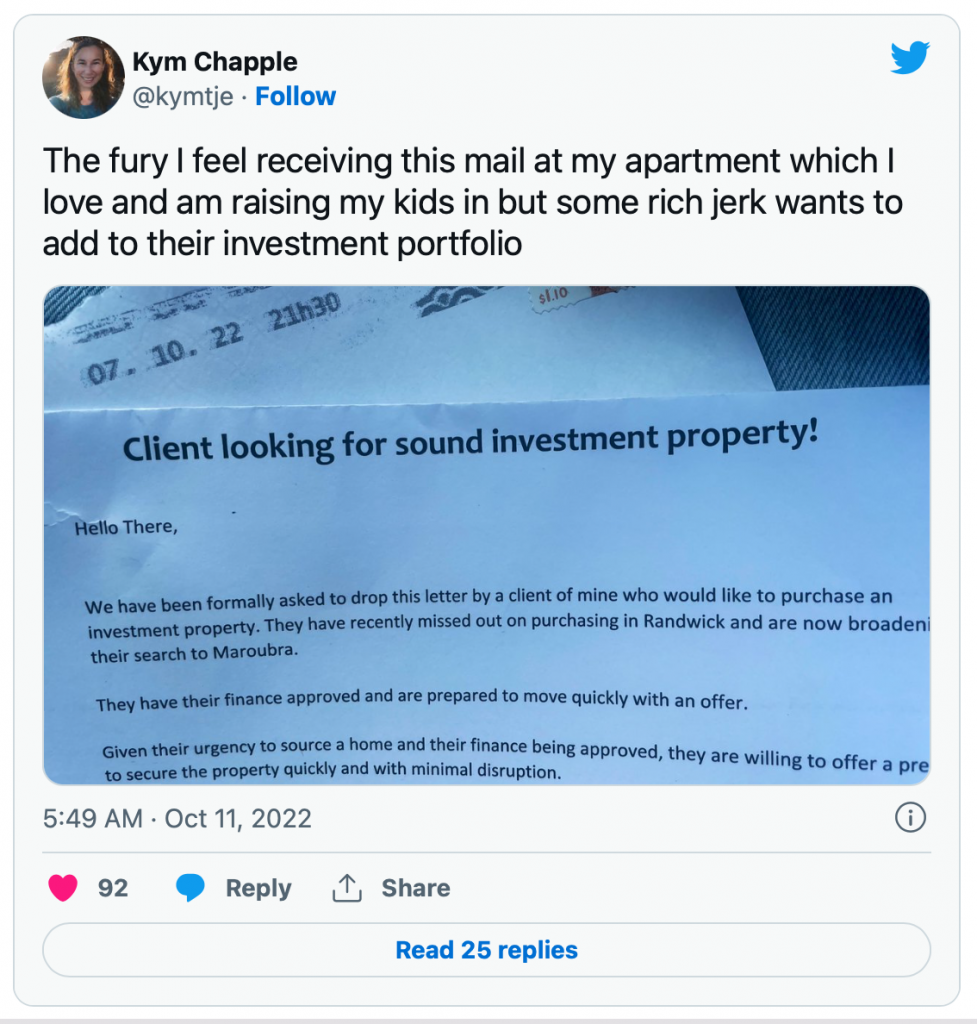

Agents in Australia are turning to increasingly frenzied measures to hunt for sellers.

Lower supply, falling house prices and rapid interest rate rises are deterring sellers from entering the market.

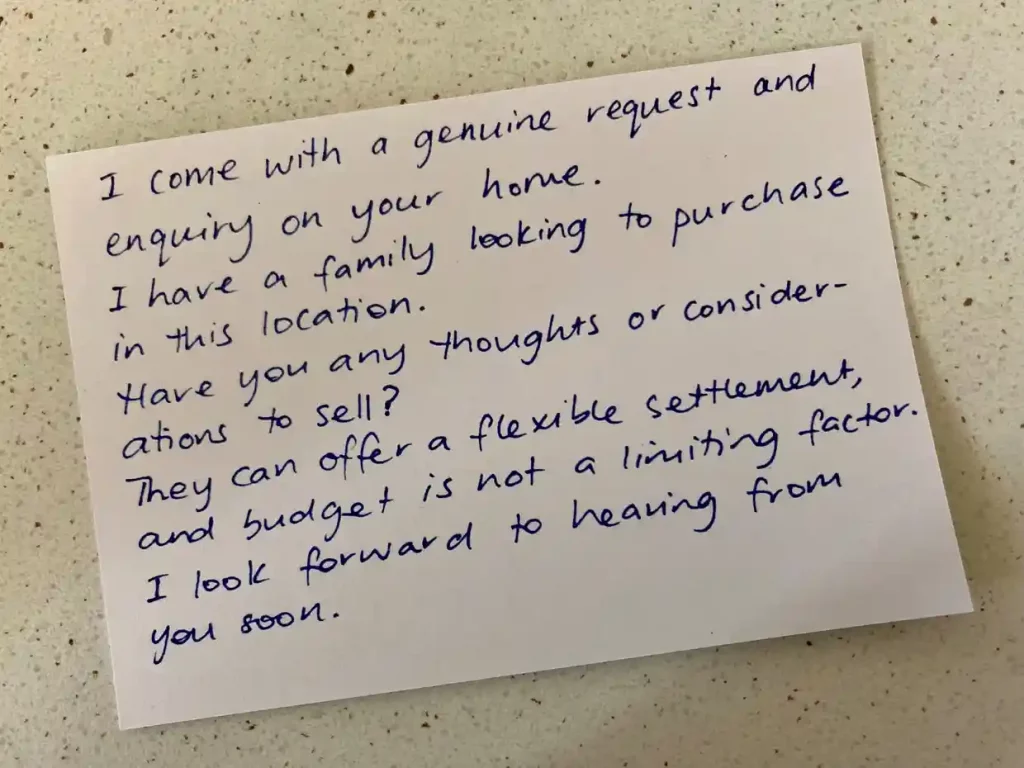

Latest tactics include handwritten “pleas”, recipe cards and even garden seeds, posted through letterboxes in an attempt to lure new prospects.

The number of newly advertised homes for sale on Realestate.com fell by 7.5% last month, the latest PropTrack Listings Report released on Wednesday found, in a sluggish start to the usually busy spring season.

The Hello Haus founder, Scott Aggett, said agents were under pressure with housing stock levels notably lower than previous years, resorting to door-knocking, cold calling and flyer drops.

“Agents are on the hunt for more quality listings to service,” he said. “Their personal income and business income will be down, due to lower trading volume and lower prices when compared with last year’s revenue.

“They need listings that are fresh and priced to today’s market value, not homes they may have been working on with vendors that have been considering selling for some time and [are] yet to adapt to current pricing levels.”

Scott Aggett, Founder Hello Haus

The unsolicited, door-to-door approach is angering some homeowners

Planting the seed

Tougher market conditions are also encouraging some agents to get in touch with their creative side to lure prospective buyers.

Some residents have reported to have been receiving three or four offers for agent evaluations a week, often accompanied by handwritten notes, recipes or garden seeds, to help seal the deal.

Some homeowners are reporting to find this approach a little “creepy”.

How far would you be prepared to go to get new clients? Let us know in the comments below.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been published from an article in The Guardian by Caitlin Cassidy on 21st October 2022. The headline and images have been changed.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

The world’s richest billionaires come from varied backgrounds, industries, generations and countries.

They’re tech entrepreneurs, a fashion magnate, probably the world’s savviest ever investor, a pioneering industrialist and a space-watching Twitter hot head – hi Elon.

What sets them apart, however, is their canny ability to make money. They’re not just good at it, they’re the best in the world at it. Possibly ever. From pioneering inventions to repeated shrewd business moves they’re billionaires for a reason.

Can we learn anything from them? Without a doubt.

Check out these pearls of wisdom from the world’s top 10 richest billionaires.

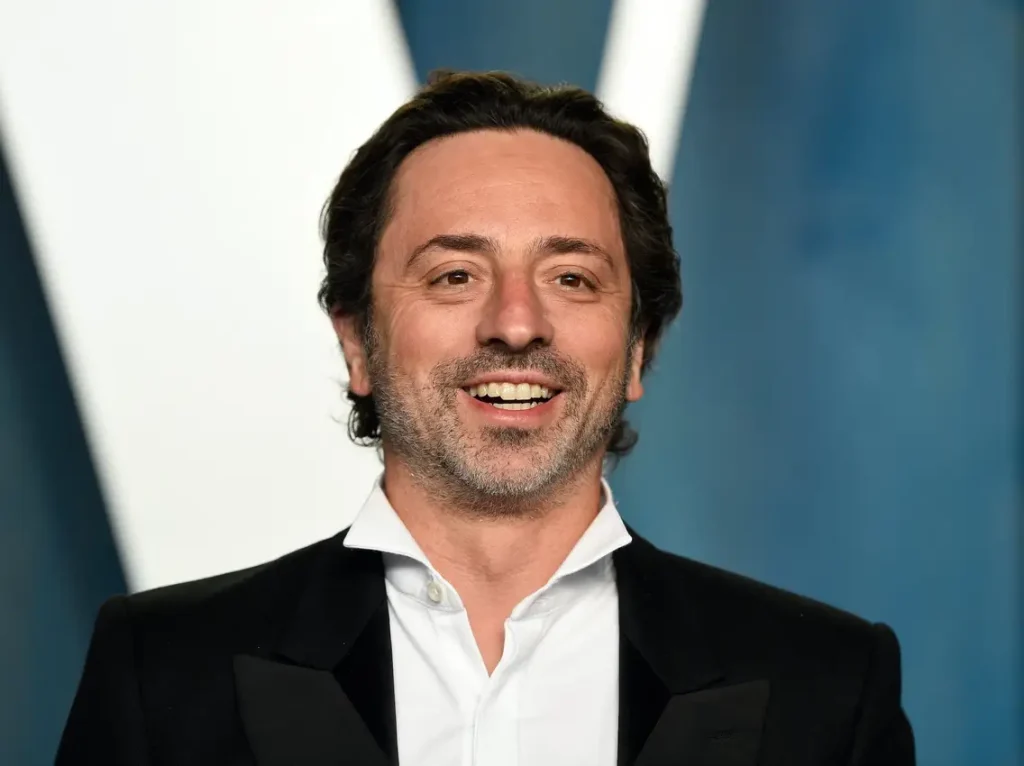

10) Sergey Brin

The computer scientist and Google co-founder is famed for creating a culture of innovation, experimentation and developing creative technology on his way to an $80.5bn fortune. The secret? Not being confined by rules, apparently.

“Too many rules stifle innovation.”

S.Brin

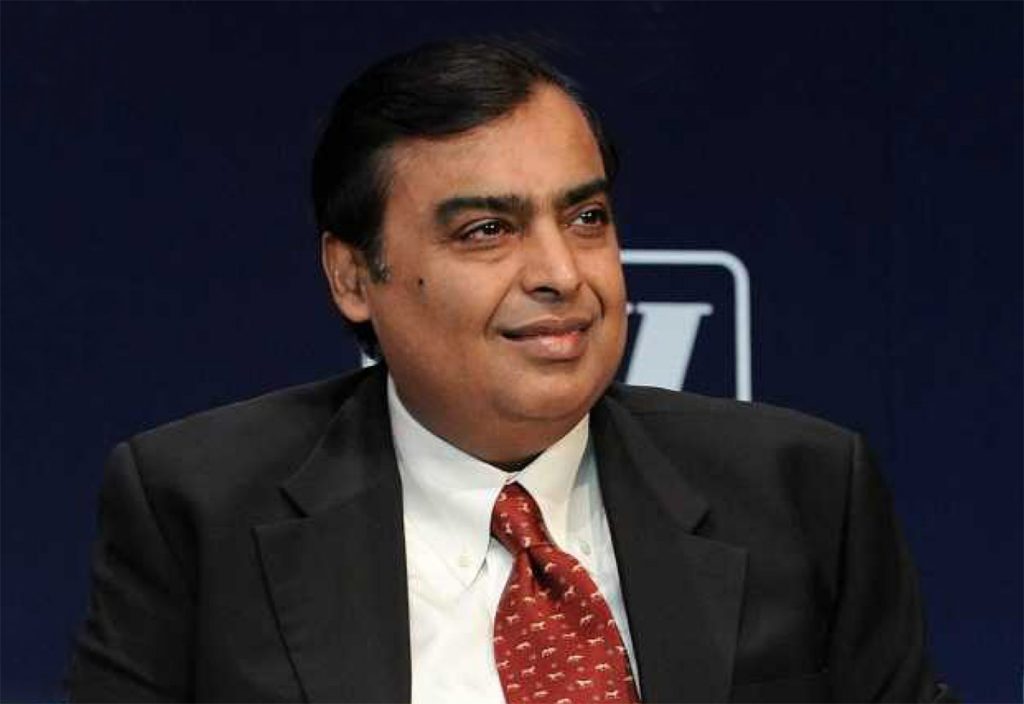

9) Mukesh Ambani

The chairman of Reliance Industries has interest in telecoms, retail, oil and gas and petrochemicals.

And he just bought Dubai’s most expensive private villa ever. FOR THE SECOND TIME.

How did he turn this into an $83.9bn fortune? Hard work. Lots of hard work.

“It is important to remember that there are no overnight successes. You will need to be dedicated, single-minded, and there is no substitute to hard work.”

M. Ambani

8) Larry Page

How do you make $84bn and become one of the world’s richest billionaires? It sounds counterintuitive, but the Google co-founder says money motivation is not the way.

“If we were motivated by money, we would have sold the company a long time ago and ended up on a beach.”

L. Page

7) Larry Ellison

Larry Ellison gave up the CEO role at Oracle nearly 10 years ago, after 37 years at the helm. Still the CTO and owner of about 35% of the company he knows the importance of being different in the boardroom and the marketplace. An $87.4bn bank balance proves him right.

“If you do everything that everyone else does in business, you’re going to lose. The only way to really be ahead is to ‘be different’.”

L.Ellison

6) Warren Buffet

The former chewing gum and door-to-door salesman has come a long way and made many billions. $95.5bn to be precise. His best rule for aspiring billionaires – don’t lose money. Simple.

“Rule No. 1 is never lose money. Rule No. 2 is never forget Rule No. 1.”

W.Buffet

5) Bill Gates

Software developer and Microsoft founder Gates has spent much of the past thirty years recognised as one of the world’s richest billionaires and is now a leading philanthropist with a personal net worth estimated at $99.8bn. Follow his advice and learn more from setbacks than success.

“Your most unhappy customers are your greatest source of learning”.

B.Gates

4) Gautam Adani

Port development business leader and industrialist Gautam Adani thinks long-term vision over short-term profit is a key characteristic of a leader. It is a belief that has carried him to a $124.4bn fortune.

“I am not attracted to those politicians who are short on vision and only want to make money. I like those who have vision.”

G.Adani

3) Jeff Bezos

Shopkeeper and online retail mogul Bezos has built Amazon into an all-conquering online shopping giant with a personal net worth estimated at $130.4bn. How? Building a reputation.

“A brand for a company is like a reputation for a person. You earn reputation by trying to do hard things well.”

J.Bezos

2) Bernard Arnault

Growth, growth, growth. If it is good enough for luxury goods specialist Bernard Arnault and his family then it is good enough for any aspiring entrepreneur or lesser billionaires. It has taken the Arnault family to an estimated $147.8bn.

“The goal of a start-up is not to stay a start-up. The goal of a start-up is to grow and to become, if possible, a large company.”

B.Arnault

1) Elon Musk

A personal fortune of $207.7bn, Tesla and SpaceX optimistic for the future the world hanging on his every tweet and the title of the world’s richest man. It is fair to say Elon Musk knows a thing or two about making money. As the quote shows he has a single-minded determination to go his own way.

“If something is important enough, even if the odds are against you, you should still do it.”

E.Musk

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been published from an article published online in Arabian Business on 16th October 2022, without modifications to the text. Only the headline has been changed.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our NewsBites blog, updated weekly.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

Investors have rained cash on Uber, Airbnb and other unprofitable companies.

Any one of these 15 money-losing companies could become the stock market’s biggest ‘unicorn’ failure ever.

David Rush holds a Guinness world record for cramming 100 candles into his mouth and lighting them.

Sandeep Singh Kaila spun a basketball on a toothbrush for a record 1 minute and 8.15 seconds. Neville Sharp emitted a 112.4 decibel burp.

If those zany stunts can make it into the Guinness Book of World Records, there should be a category for something really important — the world’s biggest startup company failure.

There is certainly no shortage of contenders for this dubious honor.

Before 2015, the biggest bankruptcies (by funding) were Solyndra ($1.2 billion), Abound Solar ($614 million), and Better Place ($675 million).

WebVan got a lot of publicity when it received $275 million in venture capital funding and failed in 2001 after three years of operation. More recently, Theranos received $500 million in venture capital funding and was a well-publicized disaster, with CEO Elizabeth Holmes and president Ramesh “Sunny” Balwani both convicted of multiple counts of fraud.

Those failures are large, but the cumulative losses of many startups that have not yet gone bankrupt are orders of magnitude larger.

The table below shows the funds raised by the 15 biggest money-losing startups in the U.S. Cumulatively they raised $93.8 billion in startup funds and have lost $135.1 billion.

Only one of these 15 companies has ever had a profitable quarter — Airbnb had a $378 million profit on $2.1 billion in revenue in the second quarter of 2022.

All of the other startups in the table have recent losses that exceed 10% of revenue and most exceed 30%.

Any hopeful arguments that profitability is just around the corner ring hollow when every company is at least nine years old and two are more than 20 years old.

At some point, investors will say, “Enough is enough” and realize that it is a sunk-cost fallacy to throw good money after bad.

Eleven of the 15 companies in the table have raised more money than was raised by any bankrupt startup.

The two biggest losers so far are Uber and WeWork.

So far, Uber has cumulative losses of $31.7 billion and WeWork $20.7 billion, with no end in sight. Uber’s stock price is down about 35% from its 52-week high. WeWork is down 71% and is now officially a penny stock.

Losses have to be financed and it is increasingly difficult for these companies to do so.

Uber has cumulative losses of $31.7 billion and WeWork $20.7 billion. Most of these so-called unicorn startups have seen their share prices fall more than 50% in the past year, and many of these stocks are down more than 90%.

Most of these so-called unicorn startups have seen their share prices fall more than 50% in the past year, and many of these stocks are down more than 90%. WeWork isn’t the only unicorn turning into a penny stock.

These stock-price declines will make it increasingly difficult and expensive to issue more stock in order to raise funds to cover ongoing losses. Meanwhile, rising interest rates are increasing the cost of servicing existing debt and making it difficult and expensive to issue even more debt.

Many unicorns will surely soon go bankrupt or be acquired at fire-sale prices. A failure of Uber or WeWork would be 10 times larger than the previous records for lost venture-capital funding.

A wave of unicorn failures would send tremors through financial markets, but it is unlikely that the federal government would use a “too-big-too-fail” excuse to intervene.

Although the startups in the table are U.S. companies, unicorn startups in other countries have similar problems: European startups (Delivery Hero DHER, -0.90%, Deliveroo ROO, –2.44%, and Wise WISE, -0.78% ); Chinese ones (Didi DIDIY, -5.50%, Kuaishou 1024, -3.44%, Billi Billi , and Pinduoduo PDD, -2.60% ); Indian ones (Ola , Paytm , and Zomato 543320, -1.29% ), and Singaporean ones (Grab and SEA ) also have multi-billion dollar cumulative losses.

New records among unicorn companies will likely soon be set all over the world — but they won’t be as benign as records for candle stuffing, basketball spinning, and burping.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

Jeffrey Lee Funk and Gary Smithwrites for Market Watch.

This story has been published from an articleon 14th September 2022, without modifications to the text. Only the headline has been changed.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

Everyone makes typos. Even the best writers get caught out. But when real estate agents are entrusted to sell properties worth millions of dollars, there really is no excuse for not paying attention to the smallest detail.

Especially with the range of technologies out there that can help. Some blunders you simply can’t ignore.

The ones that cause clients to doubt an agent’s professionalism, and reflect poorly on the agency they represent. These typos are very awkward because they are so very public.

One place where these awkward misprints are usually found is in a property’s public listing description.

Any experienced agent will tell you that the property writeup is a critical part of the listing process. An engaging description will not only set you apart from other agents and their marketing. It will serve to hook prospective leads and set you up with that all-important client relationship.

We’ve assembled a list of the most common slip-ups found in real estate write-ups.

Forget embarrassing Typos: use an AI writing assistant

Cut To Bloopers

1. SEPERATE …

Don’t be the reason to build a wall between you and your client – it should be ‘separate’

2. ACCOMODATION …

It’s a mouthful alright – it should be ‘accommodation’

3. FORMALLY…

Remember who said it first – it should be ‘formerly‘

4. PRINCIPLE…

Principles are for theoretical physicists. For foremost features – it should be ‘principal‘

5. DUEL …

Let’s hope there are no fights to settle – it should be ‘dual’

6. SORT AFTER …

If you want to remain in demand, don’t make this mistake – it should be ‘sought-after’

7. STAINLESS STEAL …

Best to not get in trouble with the law – it should be ‘steel’

8. INDEPENDANT …

Sloppy errors will have you singled out – it should be ‘independent’

9. EXTENTION …

Is this really the ‘extent’ of your spelling skills? – it should be ‘extension’

10. VOLTED …

You could be in for a shock if you get this one wrong – when it should be ‘vaulted’

Saving Face

Whilst we’re all human and make mistakes, clients are within their rights to expect their agent to cross every ‘t’ and dot every ‘i’ when transacting their home.

Sometimes the typos or grammos go unnoticed but many of them do not.

Although they may appear trivial, research has shown they can have a real impact on your credibility as a professional agent. There are plenty of other agents a client can choose from so why give them an excuse to shop around.

Grammar Rules in Real Estate

Real-estate agents better take out that red pen. An article in The Wall Street Journal quoted that:

“It’s not just English teachers who notice misspellings in luxury-home listings; typos and missing commas can slow sales and drag down prices.

An analysis of listings priced at $1 million and up shows that “perfect” listings—written in full sentences without spelling or grammatical errors—sell three days faster and are 10% more likely to sell for more than their list price.”

Sanette Tanaka Reporter, The Wall Street Journal

Write better, read better, sell faster

And for the estate agents reading this, there are some great efficiency tools to help you. Intelligently automated writing assistants like overwrite.ai mean agents no longer have to worry about silly typos or bad grammar. The agent enters the key property particulars using the intuitive, user-friendly platform, and the property description is created in seconds.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for estate agents | Sign up for your Free 7 Day Trial.

Leading AI and Tech Entrepreneurs gather in a few weeks to discuss innovation and investment, at the Middle East’s biggest technology event.

AI Everything aims to provide a nuanced understanding of the state of AI technology and it’s long-term potential, while spotlighting rising stars.

And overwrite.ai Founder and CEO Ayman Alashkar, will be speaking across 3 days of exciting panels with fellow visionaries from a range of industries.

Did you know that each year the global real estate industry wastes more than 16 million hours, and US$2.5 Billion, manually writing real estate marketing content? That’s enough to make 625 thousand trips to the Moon and back.

overwrite.ai has fixed that. We are a leading AI writing assistant for the real estate industry. An efficiency tool. Augmenting human capability by instantly creating localised, high-quality Real Estate marketing content.

And we are doing to the property marketing industry, what Docusign has done for document management. Total disruption.

“Dubai is epitomised by its passion for growth and innovation.

The AI Everything event puts Dubai on the map, highlighting the region’s enormous talent pool and potential.“

A real estate economist and AI strategist with +20years’ experience as an asset manager, investor, developer and banker, Ayman founded the business in 2020.

To learn more about us and our ground breaking technology, meet us at Za’abeel Hall 7, stand P-B126.

We’re giving away 15 FREE 5-day passes. Email us at contact@overwrite.ai for the chance to win your FREE GUEST PASS.

Meet the rising tech entrepreneurs at AI Everything and North Star

Ayman will be taking part in 3 brilliant panel sessions. Watch him on

10th October @ the 10x Stage

Panel Discussion: Funding Winter? Availability and levels from seed to C today

Is the pool of cash for startups drying up and why?

Pre-seed and seed challenges and how to get around them

Bootstrapping pros and cons

So you’re on your way: series B, series C buy in trends and downrounds

Are any verticals bucking the trend or more less impacted at least?

Win one of 15 FREE 5-day passes that we’re giving away. Email us at contact@overwrite.ai for the chance to win your FREE GUEST PASS.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for estate agents | Sign up for your Free 7 Day Trial.

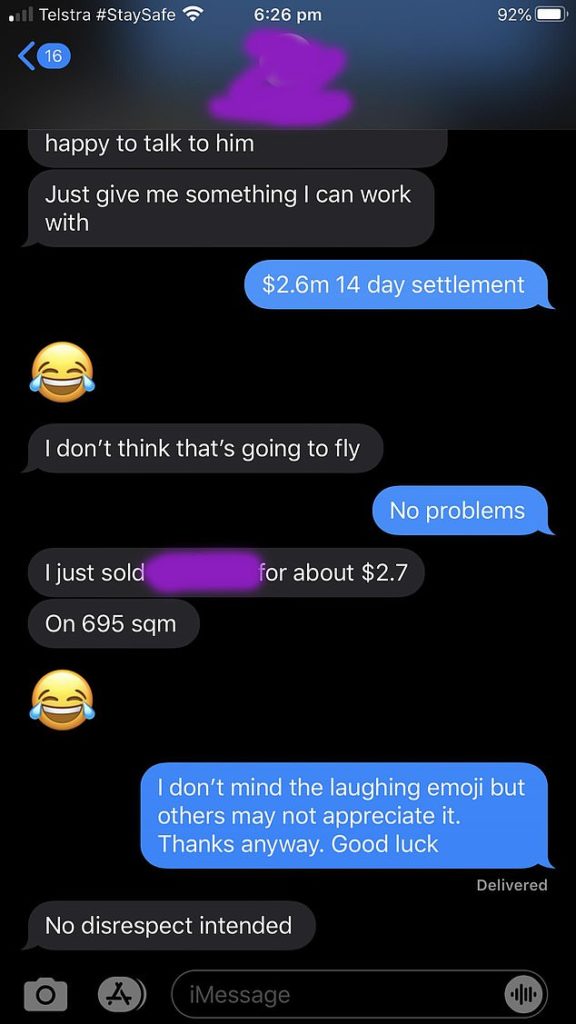

Real estate agent responded with laughing emojis to an A$2.6million offer.

An Aussie real estate agent has been slammed for sending a laughing emoji in response to a potential buyer’s offer for a multi million-dollar property in Sydney.

In a text message exchange shared on Reddit, the agent asked the potential buyer to give him an offer he could ‘work with’ for the property.

The buyer responded with an offer of A$ 2.6million dollars and a 14-day settlement period, only to be told by the agent the figure was laughable and ‘wouldn’t fly’.

‘I just sold (another property) for about A$ 2.7million, on 695 square metres,’ the agent replied, adding insult with a second laughing emoji.

How the dialogue played out…

The bidder politely replied that while the emoji didn’t offend them, it might insult other customers.

‘I don’t mind the laughing emoji but others may not appreciate it. Thanks anyway. Good luck,’ he wrote.

‘No disrespect intended,’ the agent replied.

‘An escort rejecting your mother’s credit card has more professionalism than this. Keep it up Sydney Real Estate!’ Posted the prospective home buyer alongside a screenshot of the message exchange.

Not The Only One

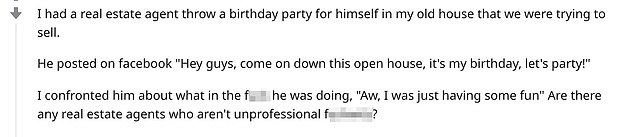

The post was flooded with stories of other shocking behaviour from other real estate agents.

One person said their real estate agent used their open home to throw himself a birthday party.

Here’s how it went:

‘He posted on Facebook ‘Hey guys, come on down this open house, it’s my birthday, let’s party!’ the person wrote.

‘I confronted him about what in the f**k he was doing, ‘Aw, I was just having some fun’.

‘Same thing happened to us bidding on a house. It was listed for “offers over A$ 610k” and we offered A$ 615k over the phone. The agent just laughed,’ another said.

‘A toddler pretending to be a real estate agent would do a better job than this,’ one said.

Say What?

How far have you gone with your responses to “silly” client offers? We’d love to hear in the comments below!

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

Eliza McPhee is a writer for Daily Mail, Australia

This story has been published from a wire agency feed without modifications to the text. Only the headline has been changed.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for estate agents | Sign up for your Free 7 Day Trial.

Ever wished that you could read your client’s mind and be one step ahead of them?

Understanding the way your client thinks is your secret weapon to bringing home that sale.

We reveal the 4 most common personality types and the clues that could help you sell to them, better.

Getting inside their minds

Experts believe that individuals are wired to make purchasing decisions, based on their personality type. Which type is your client?

1. The Leader

This client type has come prepared; they did their research, and know exactly what they’re looking for. Super motivated, they have no time for small talk, wanting to cut to the chase. They’ll make decisions quick and generally don’t have the time to deal with sales people. Be on your toes, this personality type will be the one to walk into the home, take one look around, and sign the very same day. They’ll equally walk away in an instant if you pussy-foot around.

How do you sell to the Leader?

Tune in to these behaviours quickly, or risk losing them to a competitor. If they’re a Leader type, remember they need freedom to do just that, so let them lead the conversation, and to a degree, stay out of their way. Do not hand-hold (we’re not talking literally during viewings, although that’s equally not advisable!) and give them space to absorb the product, until they’re ready to ask questions.

2. The People Person

Common traits of this client type include them being talkative, easily excited and often extroverted. Their number one need is to connect with the sales agent. As the name suggest, they’re “people-people”, and value a personal touch, so stay close (and then close).

How do you sell to the People Person?

Tip 1: Do not be pushy! Drop the sales pitch, turn off “sales mode” and turn on “relationship mode”. These customers are people-oriented, so create an environment free of confrontation or pressure.

“They enjoy the journey, have time to talk, want to get value from your expertise in the sales process, and value your knowledge in helping them make a sensible investment or find their dream home. Reinforce their beliefs, be a great listener, be available, be “with them” and support them. If you master this type and serve them really well, they’re going to be a walking, talking, billboard for you. Put lots of business cards in their hands.”

Tap in to key personality types

3. The Free Spirit

The Free Spirit is fun-loving and likes to have a good time. They’re extremely independent and are risk-takers. They are open to ideas, won’t mind being thrown a curve ball, but will be turned off by slick, rehearsed sales routines. They like to be in control of how and when things get done, so you could be in for an exhilarating but rocky ride.

How do you sell to the Free Spirit?

Get excited and celebrate with them! They’re creative people so make the sales approach equally exciting and celebratory, not boring and stale. Offer something they haven’t yet considered yet; you never know with this personality type just what might trigger that decision to buy.

4. The Task Master

The Task Master will be your most challenging personality to deal with. They are punctual, meticulous, structured, and very detail-oriented. They are the total opposite of the Free Spirit. Dependability and reliability are their biggest needs in dealing with a sales agent.

How do you sell to this Task Master?

They are cautious and need reassurance, so going in full throttle won’t work. Don’t try to pressure-sell them; they’ll just shut down. They’re going to listen to every piece of information, so make sure it’s 100% on point.

And be prepared for them having to “think about it” even after numerous conversations. The technique here is to have great follow through, stick with the plan, and unlike the Free Spirit, do not throw them any curve balls. Be dependable, and do what you said you were going to do. Eventually, your credibility and trust will win them over before the final purchasing decision.

Know yourself, too

Knowing as much as you can about your client, as quickly as you can, will be a game changer. This is as close as you’ll get to being inside your customer’s brain and know what they’re thinking, so you know what your next move is.

Yet, even armed with all this knowledge, you must also know your own personality or sales style. This will enable you to adapt your natural behaviours and manage their expectations. You’ll need to shape the relationship along the way if you want to establish effective communication.

As you get more confident, you can begin to adjust yourself, and integrate your understanding of your own personality into the sales process.

But with any human interaction, no amount of self awareness or clever second-guessing of their verbal or visual cues, will be of use if the foundations aren’t set around honestly and integrity.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for estate agents | Sign up for your Free 7 Day Trial.

To do your job effectively, you need hard skills; the technical know-how and subject-matter knowledge to fulfil your responsibilities.

But in a forever-changed world of work, lesser-touted ‘soft skills’ may be just as important – if not even more crucial.

These skills are more nuanced. Low-profile. Think personal characteristics and behaviours that make a strong leader or a good team member.

Strong Words. Softly Spoken.

Employers are increasingly considering a candidate’s soft skills as closely as their experience and explicit technical specialties.

For some people, soft skills are innate. For example, there are those for whom being a good communicator or analytical thinker, comes naturally.

But for others, developing soft skills can be more challenging. Yet it’s possible for everyone to sharpen these characteristics. And that, say experts, is something we should all be doing.

What are Soft Skills?

There is no definitive list of soft skills, but the term essentially refers to abilities beyond the technical.

Confidence with certain software, for instance, is a hard skill. On the other hand, knowing how to analyse different software packages to figure out what a company should be using requires critical thinking: a soft skill.

Another major soft-skill area is communication.

Effectively communicating with colleagues, clients and management requires dexterity and emotional intelligence. Empathy, teamwork and compassion are also skills that fall under that same umbrella.

Many soft skills are highly practical, like efficiency, prioritisation, organisation and time management – all traits that are becoming increasingly critical for remote and hybrid workers.

And soft skills aren’t merely useful at work – they’re generally invaluable. The same skills that enable workers to operate successfully within company hierarchy and rise to the top also breed successful interpersonal relationships, for instance.

A Notable Shift

As many of the highly technical parts of work are becoming increasingly automated, or replaced by technological tools, companies are instead looking for workers who can problem-solve, juggle larger responsibilities and work well with others.

Additionally, soft skills have become even more important in the post-pandemic, largely remote work landscape. For instance: communication can be much more nuanced and complex when workers don’t see colleagues face to face.

Communication can be much more nuanced and complex when workers don’t see colleagues face to face.

Adaptability, too, is a soft skill – and the past two years have called for a lot of it.

It’s not to say that technical skills have fallen by the wayside, but companies have increasingly come to realise emphasising the interpersonal skills that hold organisations together are what drives great results.

Global job site Monster’s The Future of Work 2021: Global Hiring Outlook revealed soft skills such as collaboration, teamwork, dependability and flexibility are among the skills employers most prize in workers.

Turning “Softer”

We tend to be aware of our strengths, but honing interpersonal skills starts with soliciting feedback to identify your weaknesses and blind spots. Improving them may mean forcing yourself out of your comfort zone.

If you want to improve your imaginative thinking or problem-solving, for instance, try sitting in on brainstorming sessions with the company’s creatives.

As a result, employers are actively soliciting candidates who have these intangibles. Hiring manager may ask candidates to demonstrate soft skillsets, or this “moon-shot mindset”.

For example, they may be asked to show a real-life example of passion or commitment, prove their resilience in a particularly challenging situation, or provide evidence of continuous learning at work.

To best prepare for situations like these, candidates should identify their strongest soft skills in advance, and be ready to demonstrate them.

Of course, technical skills and experience on your CV will always be important, but in the changed world of work, they’re not enough: you’ll still need to convince recruiters you possess the softer skills that will help you be a leader.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been published from an articleon 25th July 2022.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for estate agents | Sign up for your Free 7 Day Trial.

Social media marketing has engulfed the residential real estate business, providing a 24/7 reality show reel of real estate agents and their antics.

First Bloggers, then Vloggers, and now Tik-Tokers. It seems as though every agent has their finger in one or more social media pie, promoting themselves and their listings to a worldwide, property-hungry audience.

This week we’re talking Podcasts. They’re not the newest medium on the block. But they’re what growing numbers of savvy agents are turning to.

But there’s one moment in the entire MCU that, in my humble opinion, defines the #entrepreneur‘s journey better than any #influencer or #MBA course ever can.

Try. Fail. Rise. Unleash.

It’s that scene in #CaptainMarvel. When she realises that she’s been blocking herself from unleashing her full potential. Fighting with one hand tied behind her back.

She changes her psychology. Sets her mind free.

And in so doing, she unlocks the full awesomeness of her raw power.

At that point, even #chrishemsworth will probably agree that #CaptainMarvel is the most powerful of all the MCU characters.

You are where you are, doing what you are doing, because you dared.

Many of the people in your universe, haven’t dared to go it alone. To do what you’re doing. They don’t understand what it’s like. Every…single…day.

So block out the social media noise and all the social constraints.

Don’t hold back. Don’t mute yourself. Don’t doubt or deny yourself.

Don’t seek to please or to be understood.

Just get #raw! Do it as you see it. Say it as you mean it.

Unleash the truest version of yourself. Your success will follow.

NB: No cheese 🧀 was harmed in the making of this post

Ayman Alashkar is a real estate economist and AI strategist, with +20years’ experience as real estate asset manager, investor, developer and banker.

Prior to beginning his entrepreneurial journey, Ayman was Head of Real Estate for Emirates NBD’s Private Bank, where he was responsible for $2.2 Billion in UHNWI customer Assets Under Advisory. Before this, Ayman was a MENA Director of Real Estate Advisory at Global consultancy Colliers International.

Ayman has transacted and financed over US$1.5 Billion in real estate and FX investments.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for estate agents | Sign up for your Free 7 Day Trial.

The summer real estate market. Long. Quiet. Boring. Often bearing little or no fruit, by way of sales.

For many real estate agents, it can be a hard slog.

And with many people already headed overseas for long-awaited revenge travel vacations, brokers could be forgiven for expecting another slow burn this summer.

But as we head further into the hottest season of 2022, things aren’t cooling down. On the contrary. There’s been an influx of buyers and sellers across many real estate markets worldwide.

Either way, how can agents remain as competitive as possible, and stay busy, whilst the heat rises?

This week we present four tips to take advantage of during the summer, and prepare you for the win:

1. Buddy-up With a Builder

Home renovations have soared since covid. The building trade boomed as people started to prioritise time spent at home. Added to this, a shift towards remote working meant extra space was needed to accommodate the “home office”. And summer is often when a lot of home refurbs take place.

Having a close connection to a contractor will therefore keep an agent up to date with new inventory. And in case of stock drying up, having an inside guy can get you an intro before anything comes to market. Use this time to make contacts while renovation work is underway.

2. Old is Gold

Never neglect old clients.

Agents shouldn’t let any influx of new prospects distract them from tending to old clients. It’s always important to contact them. Share valuable information. Remind them why they loved working with you in the first place.

Treating these past clients right is the key to drawing new business. Referrals and word-of-mouth are the secret to success for many top agents. Pick up the phone to previous clients and say hello. If they’re taking some summer down-time, they might be in just the right mood for a chat.

3. Become Early Adopters

Technology can truly help set you apart.

AI writing assistants can instantly create your property descriptions. 3D home tours transform the online viewing experience. Digital e-signing services enable rapid, secure legal transactions. All examples of efficiency-driven technology that significantly increases the efficiency of your business.

So when it’s quiet in the office, trial some new platforms. Test out a new efficiency tool. Look at ways to save time by using intuitive and user-friendly tech. You’ll soon find that adopting an open mind will only help your business evolve.

4. Know Your Worth

While many clients are taking the reins early on, agents still play an essential role. Buying a home is a huge financial undertaking that still unnerves many. Plus, it’s impossible to think that technology can ever replace a genuine, invested, human agent.

A simple phone call. An open house. A calling card. All work wonders when delivered in the right way, at the right time. And the summer months allow you to plan all this – to perfection.

Prepare for All Weather

So as the summer season gets into full swing, let these words of wisdom stick with you:

In real estate, you don’t have to build it for them to come — you just have to make it happen for those that do. And there will always be those that do. Whatever the weather.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for estate agents | Sign up for your Free 7 Day Trial.

The MENA region’s Real Estate and Startup industries just got a massive boost from the announcement of a strategic partnership between overwrite.ai and Houza.

In a sign of maturing Proptech industry times, world-leading AI writing assistant overwrite.ai, has partnered with UAE real estate portal Houza.com, to deliver a richer online experience for industry stakeholders.

Customers of the Agency-backed disruptive portal can now use overwrite.ai to improve their consumer engagement and operational efficiency.

overwrite.ai allows them to instantly create unique, search optimised marketing content.

Founder and CEO of overwrite.ai, Ayman Alashkar said: “We’re delighted to announce our partnership with Houza and its network of leading real estate agencies.”

Agents listing with Houza now get a massive 50% discount off their subscription to overwrite.ai

“Nobody prints, then signs, scans and sends paper contracts anymore. It’s all done electronically. So why would you still write your listing descriptions manually, when you’ve got overwrite.ai to instantly do it for you, saving you time and effort?”

Ayman Alashkar – overwrite.ai

overwrite.ai is transforming how the estate agents create property write-ups

Across the industry, real estate agencies are becoming more professionally managed, organising around the core principles of efficiency and productivity.

Since its inception in 2020, overwrite.ai has sought to deliver efficiency to estate agents. It’s our centre of gravity. That’s why we’re so excited to also announce the beta-release of our CRM integration API.

Ayman Alashkar – overwrite.ai

Estate agencies can now integrate overwrite.ai with their CRM to deliver the power of AI assisted writing right where it matters most.

*Houza customers: Contact your Houza account manager to claim your overwrite.ai promo code. Applies to monthly plans only. Limited time offer. No minimum contract period required. Code valid for single use only.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for estate agents | Sign up for your Free 7 Day Trial.