Emojis are relevant as ever. If used correctly, a brand can become instantly relatable to its target audience.

A Linkedin post. An Instagram caption. An email campaign subject title.

Make no mistake – execute “emoji marketing” well, and it can have a huge impact on your marketing efforts.

But there’s a whole language behind the pretty pictures. And if you want to 1) make your content pop, 2) appear relatable and 3) reveal the “human” behind your brand, (without making any embarrassing blunders along the way), you must follow certain rules.

Your Guide to Emoji Marketing

1. Context is 🔑

It’s crucial to be mindful of cultural differences. Regardless if it’s a one-sentence tweet, or a lengthier Linkedin post. What’s a normal emoji to you could carry a different cultural connotation in another country. The linguistic context emojis carry across cultures and generations mustn’t be underestimated. Avoiding any unintentional insults or inappropriate connotations is vital.

2. A 🍑 isn’t a peach

Always look up possible risqué connotations for emojis before using them to sell your products. They can hold very different meanings. For example, a peach isn’t a peach. An eggplant isn’t an eggplant. Save yourself from getting caught up in a potentially embarrassing social media crisis, that could’ve easily been avoided with a simple Google search.

3. There is a 🕐 and 📍 for emoji use

Sometimes emojis can completely change the meaning (and tone) of a message. Some customers might feel that the use (or overuse) of emojis is frivolous or lacks professionalism. They also risk diluting the impact of your message, especially if it’s intended to be serious. Know when not to use them.

4. Test, test, and test 📝

Do your emoji-laden tweets get more engagement than text only ones? Do emojis on LinkedIn drive more clicks to articles you share? Do your followers swipe up more when you include emojis in your Instagram Stories? Test different use cases and learn from the results.

5. Research your audience 🧐

Understand your audience to see what will fly with them. Monitor their emojis and emotions to target your emoji marketing campaign and understand their sentiment towards your brand.

6. Minimal is chic ✨

Just because emojis boost engagement, you shouldn’t stuff your social post with emojis. Aside from being an aesthetic nightmare, an emoji-filled post will fetch you a one-way ticket to being trolled mercilessly online. Rightfully so. You need to know when enough is enough.

7. Beware of formatting blunders 😖

Emojis do not always look similar across different mobile devices. What’s formatted correctly on an iPhone may have weird line breaks when you check the same tweet on the desktop. Always keep this in mind while crafting content that’s dependent on a well-located emoji – it could completely ruin all your hard work and make your clients *cringe (enter appropriate *cringe emoji).

8. The Mindful Emoji user 😇

It’s not just cultures you must be aware of while using emojis. Generational differences matter as well. In essence, the next time you’re crafting content and want to use emojis, be mindful of the different connotations emojis carry across generations, as well as cultures.

Emojis are here to stay 🙏

Love them or hate them, they’re not going anywhere fast. In fact, the number of emojis available across multiple platforms and devices, seems to be ever-expanding. Understandable given the evidence that a single, cleverly placed emoji can add significant emotional cues to marketing content.

But too much of a good thing is never advisable. So use with caution. Know when enough is enough. Be mindful of your audience. Do your research. And, if you want results, it pays to be consistent, stick with what works, build momentum, and have fun along the way.

For informative news and views on the world of real estate, proptech and AI, follow overwrite on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite | real estate content creation, reimagined

According to a McKinsey study, nine out of 10 businesses think that their business model needs to change in 2023 and over half believe that they need to build new digital businesses to remain economically viable.

It’s not only the uncertainty and rising living costs making businesses rethink their digital strategy. Shifts in consumer expectations and a focus on sustainability have put further pressure on companies to innovate, and act as advocates for change.

Digital transformation has created a scenario where companies that are fast and agile stand to outlive those that aren’t.

But with so many competing priorities, how does one decide where to begin? Experts say, start with the basics.

Dust off your data

Before you even start to look at bringing in new technology, you need to inform your decision-making by gathering the right data. Many companies still struggle with disjointed or incomplete data and that can lead DX efforts astray.

Start by taking stock of the data you have. You might be collecting a lot of data from different sources that you haven’t brought together, haven’t interpreted and, therefore, you don’t know how to create value out of it. Also look at external sources. In some cases, combining data between organisations across the sector can provide insights on consumer trends that you might not otherwise have had.

Decide which tech (such as AI) can best tackle specific issues

Once you have clean and sufficient data you can think about which technologies, such as machine learning and AI, will best use it to tackle specific issues.

Invest in core capabilities

Inflationary spikes and a looming recession are making companies think about how to achieve more with less, both in terms of their labour and digital capabilities. Improvements in workforce scheduling, for example, can mitigate issues with labour shortages while automating manual tasks can increase productivity.

Ruben Schaubroeck is senior partner and leader of McKinsey’s digital practice in the UK, Ireland and Israel. He recommends taking an incremental approach, where small changes can lead to big results. “The best organisations take a domain-specific view of data, for instance customer service or digital sales, and think about how they can take an end-to-end view of that use case to show a clear impact on customers and employees.”

We often talk about digital and data teams and reskilling top management, but you also have to think about how you can retrain your workforce more broadly.

On the other hand, companies need to exercise caution about how they build their technical capabilities. While many companies oscillate between buying a single enterprise solution or building a custom solution from standalone tools, the most agile businesses usually do both. They buy into a modern enterprise solution and then use it as the foundation for all the other bolt-on pieces.

Focus on customer experience

While digital innovation occurs across sectors, B2B organisations often lag behind B2C vendors in customer experience. This needs to change.

Experience matters regardless of the type of business you run. Consumers, especially newer generations, can be unforgiving about engaging with brands if the experience isn’t enjoyable and more likely to turn away than to stay. Customers often move between different touch-points, from customer services to sales or sales to in-store, and in-store to online.

One way you can build this single customer view is to capitalise on data. Customer loyalty programmes are helping to drive this digital shift. Provided you have the necessary data, you can start thinking about how you can personalise each touchpoint to drive upsells and increase brand loyalty.

Embed digital in your corporate DNA

Digital transformation is often more about the people than the technology behind it. It’s about how you respond to risks and opportunities.

Resistance to change is the most common reason she sees DX projects fail, so it’s important to have the right talent in place. Change management is an underestimated factor in digital transformation and it needs to be a priority.

Where some businesses hire in chief technology officers to manage digital transformation, others are introducing roles such as a chief of data to manage the overall data analytics infrastructure.

Looking beyond hiring, it is vital to invest in upgrading the digital competencies of your overall workforce, at scale.

Practise good digital hygiene

Sustainability, resilience, cybersecurity and risk management are often afterthoughts in the process of implementing new digital solutions. But these elements need to be included at the beginning to build a lasting digital solution.

Does your solution allow you to be more agile in times of uncertainty? Do you have a disaster recovery plan should one of your data centres fail? Do you have a good data governance policy in place which informs your employees how to collect and use data? If the answer is no to most of these questions, you still have some ground-level work to do.

Living and breathing digital evolution

It is vital to invest in upgrading the digital competencies of your overall workforce, at scale.

Digital business transformation is a holistic approach to changing the way an organisation thinks, organises, operates and behaves. The digital strategy, in this sense, should be a living, breathing thing that evolves alongside the business.

But embarking on the DX journey requires caution. Trying to do too much too fast or doing nothing at all can both cost dearly.

Instead, examine the overall business goal to see what emerging technology, whatever your industry, can help achieve it.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been published from an article in Raconteur published on 29th November 2022.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

Make your open houses zing with holiday cheer. 🎄 Follow these handy Do’s and Don’ts!

1. DO: Make an entrance

Whatever the climate, make sure the entrance to the property is presentable. If your clients live in a cold climate, all walkways and stairs must be free of ice and snow. If you’re based in the desert (Dubai Brokers out there!), a quick sweep up of sandy doorsteps will go a long way.

2. DO: Control the temperature

Make sure the AC is turned up or heating turned on, when it’s time for the open house. If buyers are uncomfortable due to the temperature of the room, they are less likely to enjoy their viewing.

3. DO: Track the weather

If there’s a sandstorm or heatwave forecast to hit, it may be best to reschedule the open house. Make sure to keep an eye on upcoming weather warnings and be prepared with a new date.

4. DO: Deck the halls

Get into the spirit of the season. Take advantage of the holiday period by encouraging sellers to incorporate holiday décor into their open house. Twinkling Christmas lights or a scented holiday candle can welcome buyers and lift spirits.

5. DO: Write a powerful listing description

Listing descriptions these days are more than just point form lists. You need a powerful listing description! You want to engage your clients to feel excited about the home — especially about what the joy of purchasing a new home during the holidays will mean for them. Try to capture the excitement of the holidays to drive interest. Don’t have time to think of engaging words and carefully constructed sentences? This can easily be achieved using an AI writing assistant, specialised for real estate marketing.

Don’ts for holiday open houses

There are some things you definitely want to be careful of over the holidays when it comes to open houses.

1. DON’T: Overdo the holiday spirit

Holiday decorations will create a cozier atmosphere in the home, but you don’t want to overdo it. It can have the opposite effect. Anything that may distract from the home’s curb appeal – giant Santa and Rudolph inflatables, for example—should be put away until after the showing.

2. DON’T: Forget to declutter

Try not to go overboard and keep clutter to a minimum. Put away personal items, such as family photos, as they tend to distract potential buyers.

3. DON’T: Emphasize religion too heavily

Remember not everyone celebrates Christmas. There are many religions that don’t celebrate this time of year. Going overboard on religious symbols can be off-putting to some, so remind your clients to keep it tasteful despite their personal convictions.

4. DON’T: Leave presents out in the open

‘Tis the season of giving, but not to potential buyers. Make sure you pack expensive gifts and treasures away. Not only do many presents clutter the home, but they can be awkwardly personal for a new family trying to imagine their own future memories in the home.

Yes, you can sell homes over the holidays

The bottom line is, the work doesn’t stop just because the holidays are here! Use this time of year to brighten your home opens, not as an excuse to give up.

Remember, some buyers and tenants specifically look to this time of year to shop for a new property, and you might have just the one for them.

For informative and light-hearted news and views on the world of real estate, follow overwrite on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

Qatar isn’t the only country getting a giant boom in tourism thanks to its hosting of the 2022 World Cup.

The neighbouring United Arab Emirates is also set to benefit, with Dubai expected to see an estimated 1 million additional visitors during the course of the soccer tournament, according to the Dubai 6 Sports Council.

Paul Griffiths, CEO of Dubai Airports, in August called Dubai “the major gateway” to the World Cup and predicted it would see more tourists than Qatar itself.

And the city is pulling out all the stops, leveraging its reputation as a hyper-modern city more liberal and built-out than Qatar and advertising the extravagant tourist attractions it’s developed a reputation for.

Dubai “the major gateway” to the World Cup

Dubai is known for over-the-top and outlandish experiences — like its indoor ski slope complex in the desert, to the world’s tallest building and largest Ferris wheel.

With superyacht rentals, private jets and a soccer-themed hotel – Dubai is ready for the party.

It’s now added specific World Cup-themed experiences, simultaneously taking advantage of the fact that Qatar, a tiny country of 3 million people, is struggling to accommodate all its expected tourists and many of them will opt to lodge in Dubai for the matches instead.

This has been made possible by “match day air shuttles” being operated by Qatar Airlines and Dubai-based low-cost carrier FlyDubai– allowing travelers to book same-day round-trip flights from Dubai or nearby Oman to attend a match in Qatar and return in less than 24 hours.

“Only an hour away from Qatar by flight, Dubai is a familiar destination for global travelers,” Taufiq Rahim, a research fellow at the Mohammed bin Rashid School of Government, told CNBC. “Its tourism infrastructure and straightforward entry requirements make it a convenient base for World Cup fans.”

Qatar is expected to have delivered 45,000 hotel rooms in total by the start of November, according to Cushman & Wakefield Qatar, with tournament accommodation “bolstered by cruise ships, camping facilities, apartments and villas.”

Dubai, meanwhile, as a city has more than 140,000 hotel rooms, according to hotel data firm STR.

Around the UAE’s different emirates, 43 fan zones for watching matches have been set up, with some of the biggest – like Budweiser’s official BudX fan zone in Dubai Harbor – big enough to host 10,000 fans daily with matches aired on enormous 3,552 square-foot screens.

There’s even a soccer-themed hotel on Dubai’s man-made Palm archipelago, where the most dedicated fans can stay while being shuttled in and out of Doha for daily matches.

A $20,000 per night match viewing experience

Dubai’s revenue won’t just be coming from hotel stays and restaurants. Visitors to the emirate can rent superyachts running in the tens of thousands of dollars per night to watch matches while sailing through the Persian Gulf.

Xclusive Yachts, the UAE’s largest private charter yacht company, offers its most opulent seaborne experience at $20,000 per night on a trip-deck super yacht complete with a skydeck, onboard bar, skylounge, five cabins and a Michelin-starred chef serving gourmet meals.

“We are expecting a more than 300% [rise] in yacht bookings in November and December mainly due to visitors for the World Cup and Qatar who are also looking for leisure activities in Dubai,” Managing Director Amit Patel told Doha News in October.

Flight traffic is also shooting up — Dubai Airports in mid-November announced that a whopping 120 shuttle flights will fly in and out of the Dubai World Central airport each day between the tournament’s start and end dates of Nov. 20 and Dec. 18.

CEO of Flydubai, Ghaith Al Ghaith, said that nearly all of the airline’s match-day shuttle flights to Doha were at full capacity.

“This is a pattern that looks set to continue over the next couple of days and weeks,” Al Ghaith said.

Flydubai and Qatar Airways will be jointly running the match day shuttle flights between DWC and Doha. With the addition of flights from Dubai’s main airport, Dubai International (DXB), travelers can catch a flight every 30 to 50 minutes.

Private jet demand booms

Private jet charter companies have also seen a boom in business, with some fans willing to pay eye-watering sums to get to matches.

“We certainly see a great increase in traffic between Dubai and Doha over the coming month,” Oleg Kafarov, portfolio development and communications director at Dubai-based private charter jet company Jetex, told CNBC.

Prices for some private jet service packages run for 29,000 dirhams ($7,895) a seat. The flight time between Dubai and Doha is roughly an hour.

Party time

Like everything in Dubai, there’s a luxury option if you have the cash to spend. And given its reputation, we wouldn’t expect anything less as neighbours to the World Cup host.

So whether you’re partying on the ground, or taking to the skies for a taste of the live action in Qatar, it seems there’s no escaping World Cup fever and Dubai is ever-ready to get you in the spirit of the world sporting celebrations.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been published from an articleon 24th November 2022. The headline and imagery has been changed.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

Dubai’s property rent review regulations are to be shaken up. But is it for the better?

Rent reviews are currently linked to a geographically segmented rental price index. Reviews are capped in line with the average for a property’s location.

The Dubai Lands Department is rolling out a new index, said to factor specific building quality and amenities.

At first glance this looks like great news.

Vigilant. Proactive. Data-driven governance. But on reflection, could this be interventionist overkill?

Data Overload

An index comprised of such granular data becomes a mammoth task to maintain, even with the use of modern technology. Very possible that it falls on its own sword over time.

Example: A building’s owner spends millions today, completely upgrading its lift systems. How long until that Capex is reflected in the index? In real time? A month later? A year?

(More detail on how the index will be constructed and updated would help).

A Healthier Alternative?

Could we instead rely on market economics to determine rent reviews. At most, the regulator can set a cap and collar in place to protect against tenant and landlord exploitation.

Wouldn’t that be:

Less labour (and tech) intensive? Less subjective? More efficient?

All Systems Go

At the end of the day, property investment yields are a correlation between price and income. When the former is determined by free market economics, and the latter is controlled, the result is high price volatility.

The precise opposite of what a stable, healthy real estate economy needs.

Is this proposed change vigilance, or overkill?

Share your vote below 👇

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

Inflation is hitting everyone hard. Interest rates are higher than they’ve been in years. Home prices have continued to rise, and buyers have cooled on buying homes in the short term.

But there are some things that real estate agents can do now to survive, and grow business during the coming downturn.

Savvy real estate agents are preparing for the slowdown. Doing everything they can to pick up momentum and come out on the other side a leader in their market.

Looking for ways to ride out the recession?

Here’s some tips to recession-proof your business.

1. Expand your Territory

When the housing market shifts, it rarely shifts all at once and all in the same direction. Typically, a cooling off in prices and demand for homes in one sector, means an increase in another. If your local market is quiet, start by expanding your reach a little outside of your everyday transactions.

Look outside your normal geographic area and outside your normal price ranges. Find where people are still buying and selling.

You might even consider a completely different niche—like divorce leads. Done right, this can be a generous source of qualified leads that can fill your pipeline indefinitely. Visit DivorceThisHouse.com and learn the secrets to tapping into this often overlooked lead-gen source.

2. Level up your Personal Branding

Now is definitely not the time to become a secret agent. The last thing you want is to drop off the radar in your market.

Focus your marketing efforts on brand awareness and social media marketing. You want your prospects to know who you are and what you stand for. That way, when they’re ready to pull the trigger on a purchase or sale, you’ll be the person they think of.

3. Healthcheck your CRM

Let the CRM do the heavy lifting.

Your customer relationship management (CRM) should “work” your database for you. Setting up your CRM to keep track of your prospects, clients, and leads in today’s real estate space is essential.

Focus your marketing efforts on people who will need your services three, six, or even 12 months from now. That will help fill your pipeline with clients and keep your business healthy.

The CRM will act as an assistant, reminding you of important facts about your clients, what you discussed in your last conversation, and when you need to follow up. Let the technology do the heavy lifting.

4. Maintain Existing Clients

When the economy changes due to uncertain conditions, changing your approach to servicing your buyers and sellers may be necessary. Your client relationships are key at this time of transition, so showing them that you can still help them in whatever market we find ourselves in is important.

Even when the market isn’t in your client’s favour at the moment, it’s important to maintain your relationship because the market will always change, and your clients will remember loyalty.

5. Keep ahead of the (Economic) Times

It’s important to understand how an economic downturn impacts housing. If things in the real estate market go south for a little while, we likely won’t be alone. Many sectors of the economy will also contract, and it’s essential to understand the housing market in the context of the overall financial picture. Not all sectors of your market may slow down.

Companies like Keeping Current Matters provide graphics, charts, and infographics that you can add to your branding and post online. Posting relevant market insights positions you as an expert to your sphere and helps inform your community about current market conditions.

6. Connect as a Real Person

Recessions are challenging for everyone. That’s why it’s important to connect with your clients as a human who cares about them (and not just a real estate agent who wants to help with a transaction).

Inflation is high, prices for consumer good are rising astronomically and the world seems a pretty unstable place right now.

A phone call or a text checking in can go a long way. Plus, you’ll stay top of mind when those market questions come up.

If all you care about is getting their commission fee, this will soon become obvious to your clients. Genuine agents will gain the trust of clients. They’re likely to remain loyal and turn to you for unbiased advice, even if the outcome is not in their favour.

7. Focus Your Attention on Your Sphere of Influence

Switch your marketing efforts to your personal sphere of influence and develop a stronger referral base. These are people who already know and trust you; you don’t have to win them over for business—all you have to do is be present at the right time.

Spend time reaching out to them, supporting their endeavors, especially in a social setting, such as advertising for their kids’ sports programs and sponsoring events. Those relationships are key when there is a recession, and the market is slow.

Establish yourself as the hyperlocal leader of your community, allowing you to give back in a positive and productive way.

8. Make the Switch to a Nearly All-digital Operation

If you haven’t done so already, an economic slowdown is a great time to get your business caught up to the 21st century.

Take your business confidently online so that you are able to conduct business much more efficiently, in a digital space, without you having to be at the helm constantly.

If you’re lacking in certain areas, sign up for some courses to acquire these skills quickly, or talk to a colleague in your office who you know may be comfortable with these technologies.

Try streamlining processing that ordinarily take up valuable time, using technology to improve their efficiency.

For example, boring tasks such as writing listing descriptions can now be generated using AI writing assistant technology. This saves significant time as well as improving lead generation.

9. Market Your Current Listings More Aggressively

If you’ve got listings on the market when a recession hits, the race is on to move those properties before buyers retreat. With unrealistic expectations over the past several months, it’s even more important to price homes to move quickly.

By ramping up your marketing with new social postings, and unique language, can make a huge difference. Well written descriptions will entice potential buyers to view your listings, and make you stand out online.

You can also refresh your current listings instantly using overwrite.ai which allows you to regenerate property writeups, if the property is taking a while to shift.

Your pricing strategy is going to need to change too: prioritize speed to close over the final sale price. Of course, you still want to get the most you can for your sellers, but the longer a property sits on the market during lean times, the harder it becomes to sell at any price.

10. Join a Team

As a solo agent, you reap all the benefits of your hard work. On the other hand, you also shoulder all the risks if things go quiet. Joining a real estate team can provide you with a source of leads, some useful tech, a greater sphere of influence, and the financial support you may need to make it through particularly tough patches.

Over to You

Come out on the other side of the recession ahead of the game. Savvy recession-proofing strategies can set proactive real estate agents up for major success.

A financial recession and its negative consequences can have some unexpected benefits for upstart real estate agents.

Your job now is to find creative ways to demonstrate value to your sphere. Keep communicating with people, create conversations, be as visible as possible, and stay authentically human.

What other ways are you recession-proofing your real estate business? Let us know in the comments, and let’s keep the conversation going.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been published from an articleon 20th July 2022.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

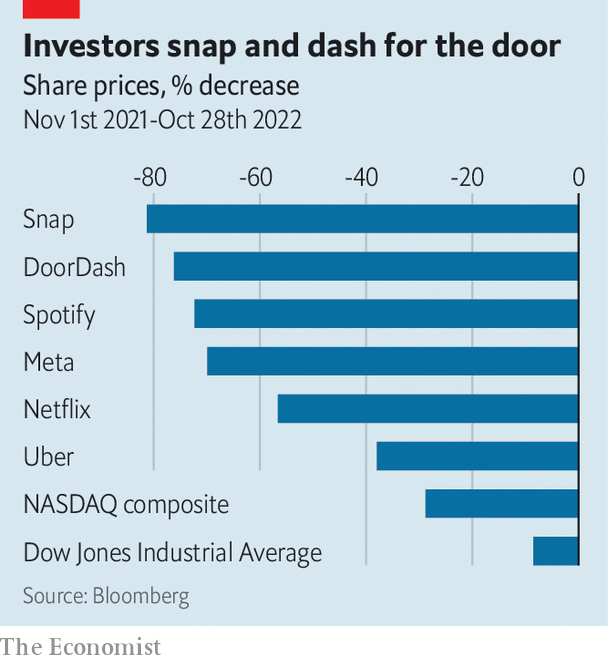

Despite superficial differences, digital darlings’ business models rest on the same shaky pillars.

When evan spiegel, boss of Snap, wrote in a leaked memo that the social-media company had been “punched in the face hard by 2022’s new economic reality”, he might as well have been describing America’s digital darlings as a whole.

After a multi-year bull run, the sector is suffering a sharp correction.

The nasdaq index, home to many consumer-internet firms, has fallen by nearly 30% in the past 12 months; the Dow Jones Industrial Average, made up of less techie firms, is down by less than 10%. Crunchbase, a data provider, estimates that American tech firms have already shed more than 45,000 jobs this year.

Macroeconomics is partly to blame. Soaring inflation and rising mortgage repayments are leading consumers to cut back on discretionary spending—and most digital offerings are discretionary.

Even the industry’s trillion-dollar giants have not been spared, despite continuing to rake in handsome profits. Alphabet, Amazon, Apple and Microsoft have collectively lost $2trn in market value over the past 12 months.

The movers, the streamers and the creepers

If you think big tech has it bad, spare a thought for the not-so-big tech. In particular, three business models embraced by firms born after the dotcom crash of 2001—and subsequently by investors—are losing steam: the movers (which shuttle people or things around cities), the streamers (which offer music and tv online) and the creepers (which make money by watching their users and selling eerily well-targeted ads). Over the past year, the firms that epitomise these business models—Uber and DoorDash; Netflix and Spotify; and Snap and Meta (which has tumbled spectacularly out of the trillion-dollar club)—have shed two-thirds of their market capitalisation on average.

And things could get worse. Despite being the global leader in ride-hailing, Uber on November 1st reported yet another quarterly loss. In its 13-year life it has torched a cumulative $25bn of cash, equivalent to roughly half its current market value. DoorDash, the leader in food delivery, also remains lossmaking. So do Spotify (despite decent revenue growth) and Snap (in addition to sharply slowing sales).

Netflix—a child of the 1990s but a streamer only since 2007—turns a profit but its revenue growth was down to 6% year on year in the third quarter, compared with a historical average of more than 20%. Meta’s revenues have now shrunk for two consecutive quarters.

On the surface, the movers, streamers and creepers—and thus their problems—look distinct. On closer inspection, though, their businesses all turn out to face the same main pitfalls: a misplaced faith in network effects, low barriers to entry and a dependence on someone else’s platform.

The network effects

Start with network effects, or “flywheels” in Silicon Valley speak—the idea that a product’s value to a user rises with the number of users. Once the user base passes a certain threshold, the argument goes, the flywheel powers a self-perpetuating cycle of growth. It also explains why so many startups seek growth at all cost, spending millions acquiring ever more customers to get the flywheel spinning.

Network effects are real. But they also have their limits. Uber believed that its headstart in ride-hailing gave it a ticket to riches, as more riders and drivers would mean less idle time for both, drawing ever more users into an unstoppable vortex. Instead, it encountered diminishing returns to scale: reducing average wait times from two minutes to one would require twice as many drivers, even though most riders would barely notice the difference. DoorDash’s hungry consumers likewise only require so many alternative Indian restaurants to choose from. And what network effects the movers enjoy are local; a user in New York cares little about the popularity of the app in Los Angeles.

The Netflix Movie scored a rare 0% audience rating on Rotten Tomatoes

Spotify and Netflix also tried to capitalise on network effects, as oodles of data on the listening and viewing habits of similar users promised to deliver an unbeatable product. Belief that Netflix’s trove of user information would give it a winning edge in creating content has been shattered by flops like “True Memoirs of an International Assassin”, which scored a rare 0% audience rating on Rotten Tomatoes, a review website. For the creepers—whose social networks are a network-effects business par excellence—the worry is what happens if the flywheels start spinning in reverse. Meta had a scare in the fourth quarter of 2021, when it lost 1m users. That loss did not turn into a stampede; the company has added users since. Next time it may not be so lucky.

From Boon to Bane

The second problem—low barriers to entry—also looks like a supposed boon that turned into a bane. Advances in technology, from smartphones to cloud computing, allowed all manner of startups, including the movers, streamers and creepers, to build consumer software cheaply and quickly. But that also meant that copycats soon emerged, and easy money allowed them to offer generous discounts to quickly build the minimum necessary scale.

Fending off the rivals

Although Uber faces only one real ride-hailing rival, Lyft, in its home market, its global expansion almost immediately ran up against local rivals such as Didi in China or Grab and Gojek in South-East Asia.

The combination of relatively simple products and free-of-charge user experience means a new twist on social media can be enough for a new challenger to gain momentum: just try to pry a teenager from TikTok.

The barriers to entry for the streamers are higher—Netflix and Spotify spend a lot of money making or licensing content. But they are not insurmountable, especially for deep-pocketed rivals. To fend off the challenge from Disney, which is spending a total of $30bn a year on content, Netflix has to keep splurging, too, to the tune of around $17bn a year. Like customer-acquisition costs for the movers, content costs eat into streamers’ profits. Disney’s streaming services lost $1.1bn in the second quarter of this year and the company has said that its Disney+ platform expects to lose money until 2024. Heavy investment explains why Netflix’s free cashflow (the money companies generate after subtracting capital investments) is equal to only 6% of revenue.

Is the clock ticking for TikTok?

The third flaw common to the three wobbly business models is their reliance on distribution platforms that are not their own. Uber and DoorDash pay a handsome fee to advertise on the iPhone and Alphabet’s Android app stores. Spotify forks over a 15% commission on subscriptions purchased on iPhones—a tax so annoying that it has filed a complaint against Apple over it. Netflix avoids the commission by forcing users to subscribe through their web browser, shifting the irritation to the customer—and quite possibly missing out on subscriptions.

Worst affected by the lack of their own rails are the creepers. Their dependence on the iPhone-Android duopoly is an existential threat. Apple’s newish requirement that users give iPhone apps permission to track their activity across other apps and websites, a move since replicated by Alphabet, may this year cost Meta an estimated $10bn in forgone revenue. Parler, a creeper favoured by the far right for its liberal attitude to speech norms, was temporarily suspended by both Apple and Android. If American national-security hawks worried about TikTok’s Chinese ownership get their way and force Apple and Alphabet to expel it from their app stores, the rising star of social media could find itself similarly thwacked.

The different business models do not face an equal balance of challenges. The movers would be in better nick if the industry had meaningful barriers to entry. The streamers may have been able to bat away new entrants if network effects had been stronger. And the creepers were in reasonable shape until Apple and Alphabet spoiled their party. One shaky pillar is problematic enough. Three of them is a disaster waiting to happen.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been repurposed from an article published online in The Economist on 31st October 2022, without modifications to the text.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our NewsBites blog, updated weekly.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

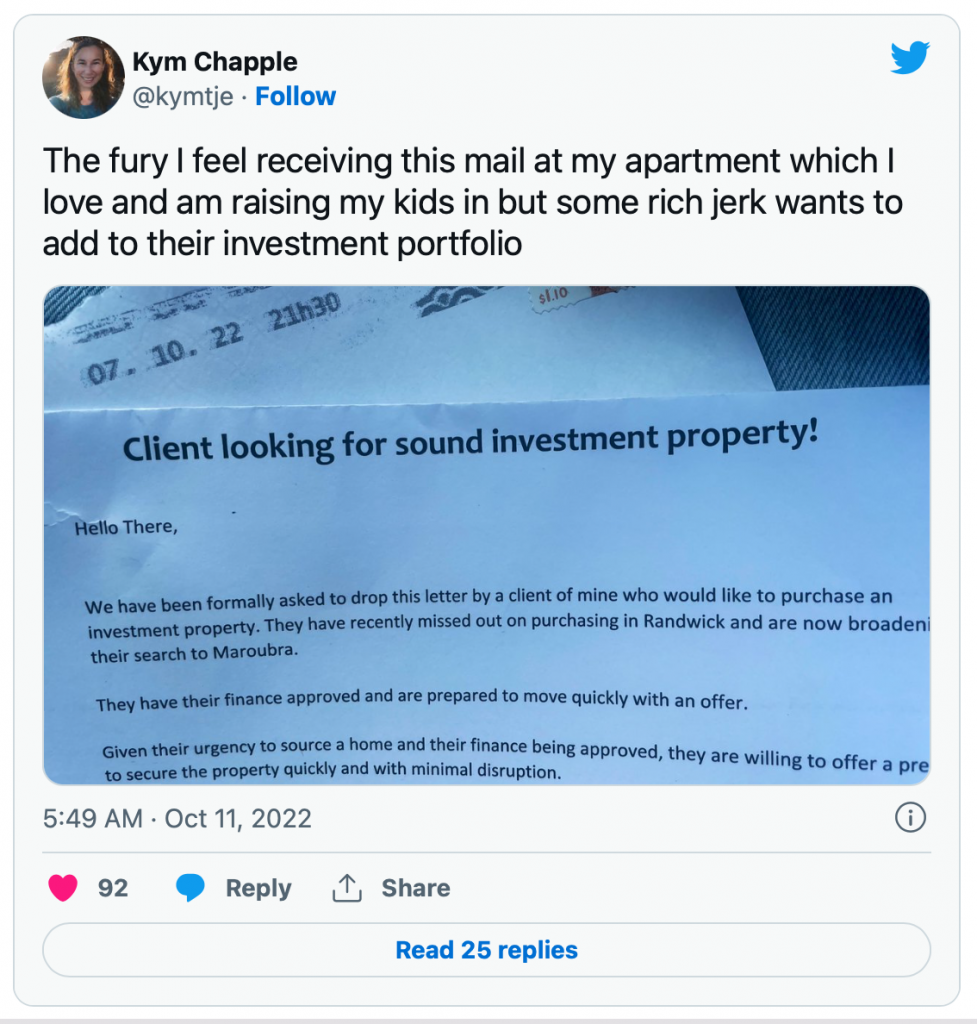

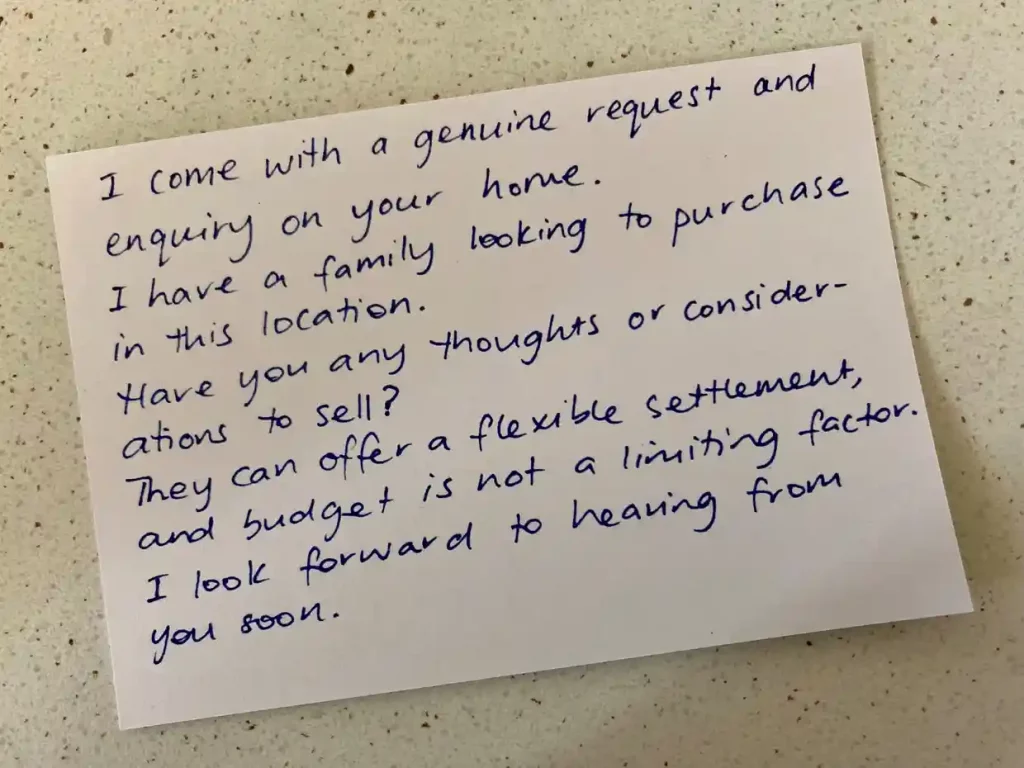

Agents in Australia are turning to increasingly frenzied measures to hunt for sellers.

Lower supply, falling house prices and rapid interest rate rises are deterring sellers from entering the market.

Latest tactics include handwritten “pleas”, recipe cards and even garden seeds, posted through letterboxes in an attempt to lure new prospects.

The number of newly advertised homes for sale on Realestate.com fell by 7.5% last month, the latest PropTrack Listings Report released on Wednesday found, in a sluggish start to the usually busy spring season.

The Hello Haus founder, Scott Aggett, said agents were under pressure with housing stock levels notably lower than previous years, resorting to door-knocking, cold calling and flyer drops.

“Agents are on the hunt for more quality listings to service,” he said. “Their personal income and business income will be down, due to lower trading volume and lower prices when compared with last year’s revenue.

“They need listings that are fresh and priced to today’s market value, not homes they may have been working on with vendors that have been considering selling for some time and [are] yet to adapt to current pricing levels.”

Scott Aggett, Founder Hello Haus

The unsolicited, door-to-door approach is angering some homeowners

Planting the seed

Tougher market conditions are also encouraging some agents to get in touch with their creative side to lure prospective buyers.

Some residents have reported to have been receiving three or four offers for agent evaluations a week, often accompanied by handwritten notes, recipes or garden seeds, to help seal the deal.

Some homeowners are reporting to find this approach a little “creepy”.

How far would you be prepared to go to get new clients? Let us know in the comments below.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been published from an article in The Guardian by Caitlin Cassidy on 21st October 2022. The headline and images have been changed.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

The world’s richest billionaires come from varied backgrounds, industries, generations and countries.

They’re tech entrepreneurs, a fashion magnate, probably the world’s savviest ever investor, a pioneering industrialist and a space-watching Twitter hot head – hi Elon.

What sets them apart, however, is their canny ability to make money. They’re not just good at it, they’re the best in the world at it. Possibly ever. From pioneering inventions to repeated shrewd business moves they’re billionaires for a reason.

Can we learn anything from them? Without a doubt.

Check out these pearls of wisdom from the world’s top 10 richest billionaires.

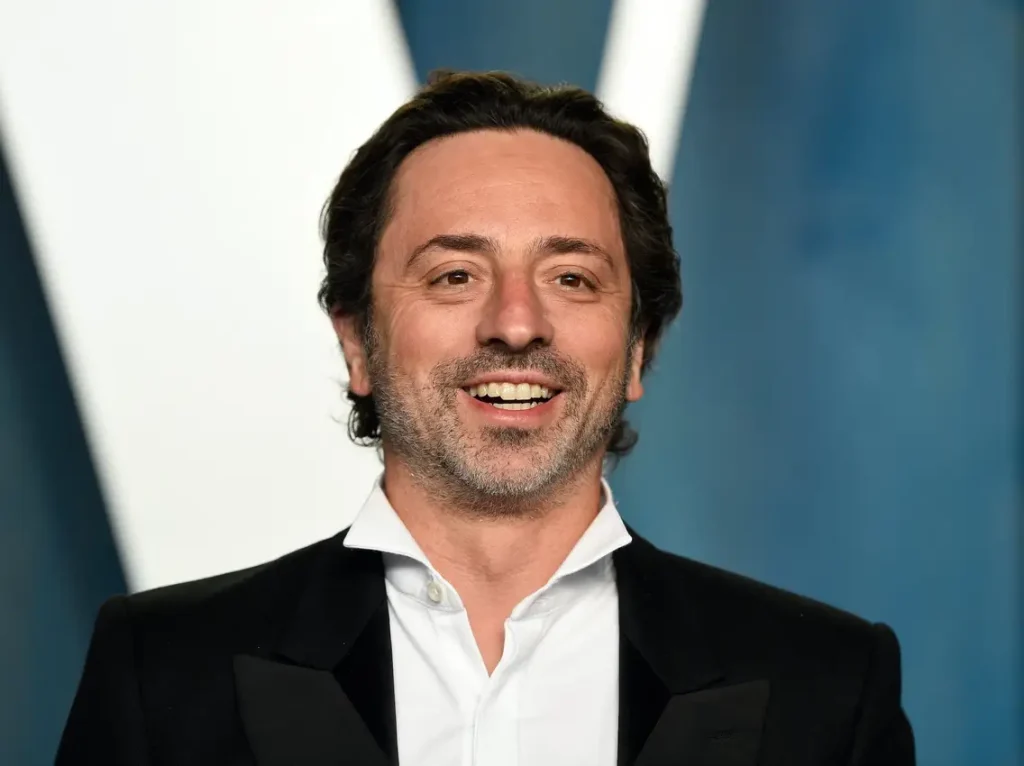

10) Sergey Brin

The computer scientist and Google co-founder is famed for creating a culture of innovation, experimentation and developing creative technology on his way to an $80.5bn fortune. The secret? Not being confined by rules, apparently.

“Too many rules stifle innovation.”

S.Brin

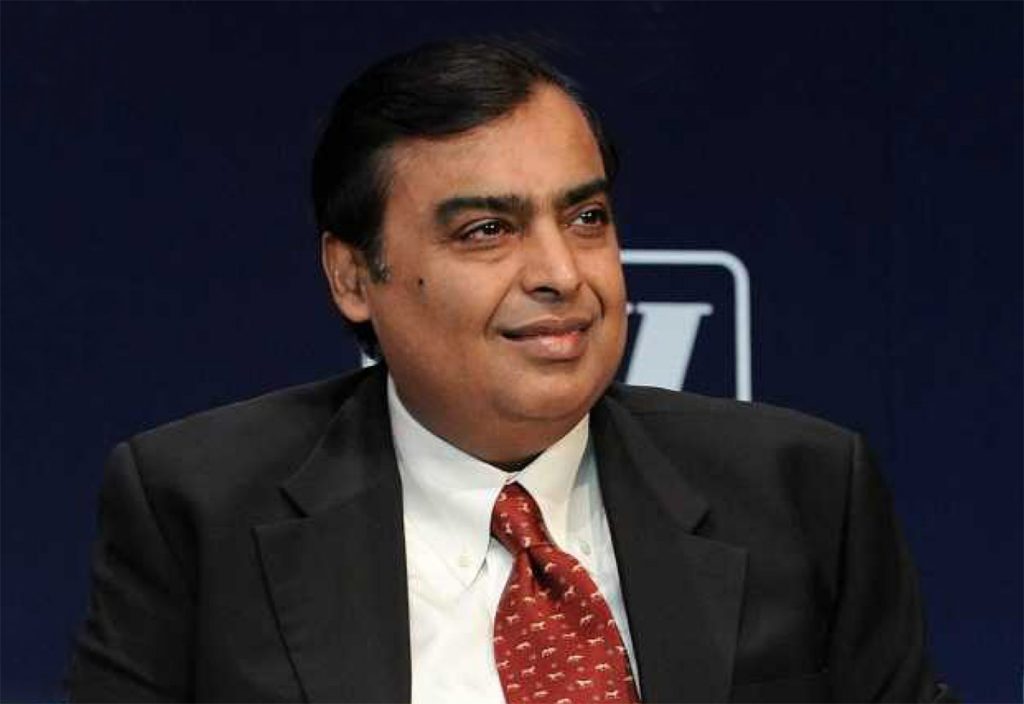

9) Mukesh Ambani

The chairman of Reliance Industries has interest in telecoms, retail, oil and gas and petrochemicals.

And he just bought Dubai’s most expensive private villa ever. FOR THE SECOND TIME.

How did he turn this into an $83.9bn fortune? Hard work. Lots of hard work.

“It is important to remember that there are no overnight successes. You will need to be dedicated, single-minded, and there is no substitute to hard work.”

M. Ambani

8) Larry Page

How do you make $84bn and become one of the world’s richest billionaires? It sounds counterintuitive, but the Google co-founder says money motivation is not the way.

“If we were motivated by money, we would have sold the company a long time ago and ended up on a beach.”

L. Page

7) Larry Ellison

Larry Ellison gave up the CEO role at Oracle nearly 10 years ago, after 37 years at the helm. Still the CTO and owner of about 35% of the company he knows the importance of being different in the boardroom and the marketplace. An $87.4bn bank balance proves him right.

“If you do everything that everyone else does in business, you’re going to lose. The only way to really be ahead is to ‘be different’.”

L.Ellison

6) Warren Buffet

The former chewing gum and door-to-door salesman has come a long way and made many billions. $95.5bn to be precise. His best rule for aspiring billionaires – don’t lose money. Simple.

“Rule No. 1 is never lose money. Rule No. 2 is never forget Rule No. 1.”

W.Buffet

5) Bill Gates

Software developer and Microsoft founder Gates has spent much of the past thirty years recognised as one of the world’s richest billionaires and is now a leading philanthropist with a personal net worth estimated at $99.8bn. Follow his advice and learn more from setbacks than success.

“Your most unhappy customers are your greatest source of learning”.

B.Gates

4) Gautam Adani

Port development business leader and industrialist Gautam Adani thinks long-term vision over short-term profit is a key characteristic of a leader. It is a belief that has carried him to a $124.4bn fortune.

“I am not attracted to those politicians who are short on vision and only want to make money. I like those who have vision.”

G.Adani

3) Jeff Bezos

Shopkeeper and online retail mogul Bezos has built Amazon into an all-conquering online shopping giant with a personal net worth estimated at $130.4bn. How? Building a reputation.

“A brand for a company is like a reputation for a person. You earn reputation by trying to do hard things well.”

J.Bezos

2) Bernard Arnault

Growth, growth, growth. If it is good enough for luxury goods specialist Bernard Arnault and his family then it is good enough for any aspiring entrepreneur or lesser billionaires. It has taken the Arnault family to an estimated $147.8bn.

“The goal of a start-up is not to stay a start-up. The goal of a start-up is to grow and to become, if possible, a large company.”

B.Arnault

1) Elon Musk

A personal fortune of $207.7bn, Tesla and SpaceX optimistic for the future the world hanging on his every tweet and the title of the world’s richest man. It is fair to say Elon Musk knows a thing or two about making money. As the quote shows he has a single-minded determination to go his own way.

“If something is important enough, even if the odds are against you, you should still do it.”

E.Musk

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

This story has been published from an article published online in Arabian Business on 16th October 2022, without modifications to the text. Only the headline has been changed.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our NewsBites blog, updated weekly.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.

Investors have rained cash on Uber, Airbnb and other unprofitable companies.

Any one of these 15 money-losing companies could become the stock market’s biggest ‘unicorn’ failure ever.

David Rush holds a Guinness world record for cramming 100 candles into his mouth and lighting them.

Sandeep Singh Kaila spun a basketball on a toothbrush for a record 1 minute and 8.15 seconds. Neville Sharp emitted a 112.4 decibel burp.

If those zany stunts can make it into the Guinness Book of World Records, there should be a category for something really important — the world’s biggest startup company failure.

There is certainly no shortage of contenders for this dubious honor.

Before 2015, the biggest bankruptcies (by funding) were Solyndra ($1.2 billion), Abound Solar ($614 million), and Better Place ($675 million).

WebVan got a lot of publicity when it received $275 million in venture capital funding and failed in 2001 after three years of operation. More recently, Theranos received $500 million in venture capital funding and was a well-publicized disaster, with CEO Elizabeth Holmes and president Ramesh “Sunny” Balwani both convicted of multiple counts of fraud.

Those failures are large, but the cumulative losses of many startups that have not yet gone bankrupt are orders of magnitude larger.

The table below shows the funds raised by the 15 biggest money-losing startups in the U.S. Cumulatively they raised $93.8 billion in startup funds and have lost $135.1 billion.

Only one of these 15 companies has ever had a profitable quarter — Airbnb had a $378 million profit on $2.1 billion in revenue in the second quarter of 2022.

All of the other startups in the table have recent losses that exceed 10% of revenue and most exceed 30%.

Any hopeful arguments that profitability is just around the corner ring hollow when every company is at least nine years old and two are more than 20 years old.

At some point, investors will say, “Enough is enough” and realize that it is a sunk-cost fallacy to throw good money after bad.

Eleven of the 15 companies in the table have raised more money than was raised by any bankrupt startup.

The two biggest losers so far are Uber and WeWork.

So far, Uber has cumulative losses of $31.7 billion and WeWork $20.7 billion, with no end in sight. Uber’s stock price is down about 35% from its 52-week high. WeWork is down 71% and is now officially a penny stock.

Losses have to be financed and it is increasingly difficult for these companies to do so.

Uber has cumulative losses of $31.7 billion and WeWork $20.7 billion. Most of these so-called unicorn startups have seen their share prices fall more than 50% in the past year, and many of these stocks are down more than 90%.

Most of these so-called unicorn startups have seen their share prices fall more than 50% in the past year, and many of these stocks are down more than 90%. WeWork isn’t the only unicorn turning into a penny stock.

These stock-price declines will make it increasingly difficult and expensive to issue more stock in order to raise funds to cover ongoing losses. Meanwhile, rising interest rates are increasing the cost of servicing existing debt and making it difficult and expensive to issue even more debt.

Many unicorns will surely soon go bankrupt or be acquired at fire-sale prices. A failure of Uber or WeWork would be 10 times larger than the previous records for lost venture-capital funding.

A wave of unicorn failures would send tremors through financial markets, but it is unlikely that the federal government would use a “too-big-too-fail” excuse to intervene.

Although the startups in the table are U.S. companies, unicorn startups in other countries have similar problems: European startups (Delivery Hero DHER, -0.90%, Deliveroo ROO, –2.44%, and Wise WISE, -0.78% ); Chinese ones (Didi DIDIY, -5.50%, Kuaishou 1024, -3.44%, Billi Billi , and Pinduoduo PDD, -2.60% ); Indian ones (Ola , Paytm , and Zomato 543320, -1.29% ), and Singaporean ones (Grab and SEA ) also have multi-billion dollar cumulative losses.

New records among unicorn companies will likely soon be set all over the world — but they won’t be as benign as records for candle stuffing, basketball spinning, and burping.

This column does not necessarily reflect the opinion of overwrite.ai and its owners.

Jeffrey Lee Funk and Gary Smithwrites for Market Watch.

This story has been published from an articleon 14th September 2022, without modifications to the text. Only the headline has been changed.

For informative and light-hearted news and views on the world of real estate, follow overwrite.ai on Instagram and LinkedIn, and keep up-to-date with our weekly NewsBites blog.

overwrite.ai | the AI writing assistant for real estate | Sign up for your Free 7 Day Trial.